Authored by Tyler Durden via Zerohedge

Pitching hedges when the market is in the middle of a blow off top is a tough sell. But, according to Chris Metli, executive director in Morgan Stanley’s Inst. Equity Division, that’s exactly what traders should be doing, for three reasons: 1) positioning, 2) pricing, and 3) potential catalysts, which “all suggest now is an attractive time to buy Feb puts as a hedge – and it is a rare event when all align.”

Here is how one of the top Morgan Stanley cross-asset quants justifies his reasoning:

First this is not a call for the final top – positive sentiment and positioning can have momentum of their own and absent some kind of shock likely take the market higher. But the rally is getting more fragile – as MS Equity Strategist Mike Wilson notes in Weekly Warm-up: Euphoria! (Jan 16, 2018) “The bottom line is that we have entered the late cycle euphoria stage we predicted a year ago.” and “it is more likely the S&P 500 will reach our bull case of 3,000 before it’s over. We just want to make sure investors appreciate this is higher, not lower risk than the rally we experienced last year.”

- The rally is getting riskier because of positioning – investors have aggressively chased beta with both futures and options. Over the last two weeks investors have bought the 2nd largest amount of S&P 500 futures (as measured by MS Trade Pressure) since at least 2010, while at the same time net holdings of S&P 500 calls are the highest and the net holdings of S&P 500 puts are the lowest since at least 2010.

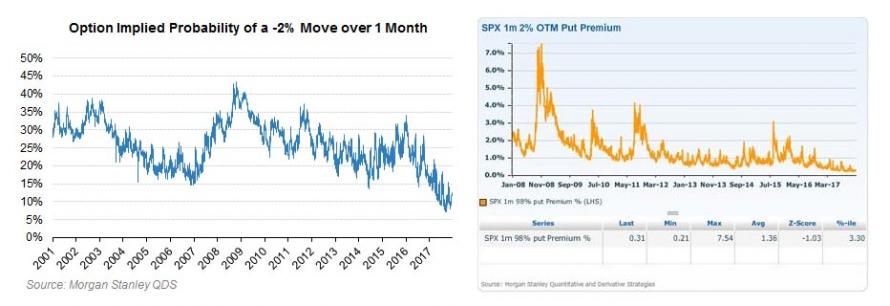

- That demand for upside and lack of interest in protection has driven short dated skew down to near post crisis lows, making puts cheaper. This flattening of skew is a sharp turnaround from the historical highs seen just last October and bucks the structural steepening of the last several years (chart above).

On one hand the flattening simply reflects a lack of demand for puts. But it also reflects the fact that volatility is now positively correlated to spot – i.e. volatility has been rising in an up market – and a belief by market participants that vol is unlikely to rise significantly if spot falls.

While this may hold for small declines in spot, QDS thinks that anything more than a 2% drawdown could drive a meaningful increase in vol, making puts even more valuable. A 2% decline would certainly surprise the market, and would also be compounded by dealer demand for options – while the overall investor community doesn’t own a lot of protection, there has been some lumpy buying of puts that means in a move lower dealers will get shorter vol and need to cover (i.e. buy options).

3) Finally there is actually a potential catalyst with a potential government shutdown this Friday January 19th, as well as the State of the Union on the 30th. Shutdowns rarely have any lasting impact, but historically have resulted in short-term equity drawdowns, and it appears that the probability of an adverse outcome this time around is rising.

To position for a quick pullback QDS suggests simply buying Feb 2% OTM SPY puts for ~41bps (272 strike vs 277.92 ref as of Friday’s close, but should roll up to higher strike on today’s rally) to capture both potential catalysts and leave a little time value to benefit from a potential increase in volatility on a selloff. The market implied probability of a 2% decline over the next month is only ~12%, in the 3rd percentile since 2001, and puts have rarely been cheaper. The MS Index Trading desk has also commented on the attractiveness of SPX hedges.

The risk of loss in the trading of stocks, options, futures, foreign exchanges, foreign equities, and bonds can be substantial and is not suitable for all investors. Trading on margin or the use of leverage is not suitable for all investors and losses exceeding your initial deposit is possible. Supporting documentation is available upon request. Trading futures, options on futures, and foreign exchanges involves substantial risk of loss and is not suitable for all investors. Carefully consider whether trading is suitable for you in light of your circumstances, knowledge, and financial resources and only risk capital should be used. Opinions, market data, and recommendations are subject to change at any time. The lower the margin used the higher the leverage and therefore increases your risk. Past performance is not necessarily indicative of future results.

Recent Comments