On January 26, 2017, with the S&P at an all-time-high, Bank of America made an unsettling announcement: a powerful sell signal, based on its quant-developed Bull Bear Indicator, was triggered.

What makes this indicator something of interest is its track record; one that supposedly had demonstrated a stunningly accurate track record for predicting size and relative timing (within a three-month time frame).

As it turned out, the Bull Bear Indicator forecasted the 12% drop that subsequently took place in early February. Was that an accurate prediction, or pure coincidence?

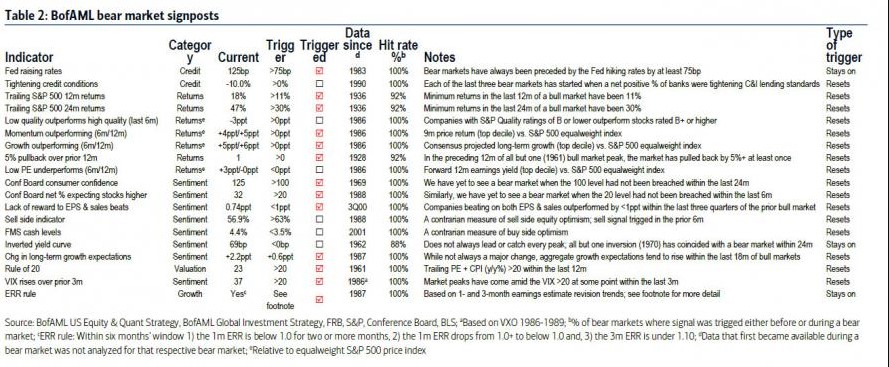

The indicator has a set of 19 criteria which are analyzed to measure the potential for a bullish or bearish market turn. When these conditions accumulate, they trigger a warning signal that a market turn is imminent.

In January of this year, 11 of those 19 conditions were occurring, prompting BofA to announce its conclusion that “a tactical S&P 500 pullback to 2686 in Feb/Mar now very likely.”

Source: BofAML Global investment Strategy

As of this week, the indicator is once again sensing an accumulation: 13 of the 19 conditions have been triggered.

Here’s the full list:

Source: BofAML US Equity and Quant Strategy via Zerohedge

A breakdown of what had already been triggered:

- Bear markets have always been preceded by the Fed hiking rates by at least 75bp from the cycle trough.

- Minimum returns in the last 12m of a bull market have been 11%.

- Minimum returns in the last 24m of a bull market have been 30%.

- 9m price return (top decile) vs. S&P 500 equal weight index.

- Consensus projected long-term growth (top decile) vs. S&P 500 equal weight index.

- We have yet to see a bear market when the 100 level had not been breached in the prior 24m.

- Similarly, we have yet to see a bear market when the 20 level had not been breached in the prior 6m.

- Companies beating on both EPS & Sales outperformed the S&P 500 by less than 1ppt within the last three quarters.

- While not always a major change, aggregate growth expectations tend to rise within the last 18m of bull markets.

- Trailing PE + CPI y/y% >20 in the prior 12m.

- Based on 1- and 3-month estimate revision trends; see footnote for more detail.

- Trailing PE + CPI (y/y%) >20 within the last 12m.

- In the preceding 12m of all but one (1961) bull market peak, the market has pulled back by 5%+ at least once.

The remaining six:

- Each of the last three bear markets has started when a net positive % of banks were tightening C&I lending standards.

- Companies with S&P Quality ratings of B or lower outperform stocks rated B+ or higher.

- Forward 12m earnings yield (top decile) vs. S&P 500 equal weight index.

- A contrarian measure of sell side equity optimism; sell signal triggered in the prior 6m.

- A contrarian measure of buy side optimism.

- Does not always lead or catch every peak and all but one inversion (1970) has coincided with a bear market within 24m.

In light of this data, the investors are probably asking themselves: “what should we I about it?”.

Here’s what Bank of America has to say:

“Our US Regime Model, a quantitative framework for stock-picking, suggests we are in the mid to late stages of the market cycle and in this stage, momentum is the best way to invest. As contrarian value investors, this is not an easy call to make. But if this bull market is closer to over, our analysis of factor returns indicates that late-stage bull markets have been dominated by stocks with strong price momentum and growth, while value, analyst neglect, and dividend yield have been the worst-performing factors.”

In other words, it’s all about “momentum” as fundamental factors no longer mean much at this juncture.

However, trading a market’s momentum is a high-risk endeavor, as there are no rational–i.e. fundamental–factors to accurately analyze turns in sentiment.

The risk of loss in the trading of stocks, options, futures, foreign exchanges, foreign equities, and bonds can be substantial and is not suitable for all investors. Trading on margin or the use of leverage is not suitable for all investors and losses exceeding your initial deposit is possible. Supporting documentation is available upon request. Trading futures, options on futures, and foreign exchanges involves substantial risk of loss and is not suitable for all investors. Carefully consider whether trading is suitable for you in light of your circumstances, knowledge, and financial resources and only risk capital should be used. Opinions, market data, and recommendations are subject to change at any time. The lower the margin used the higher the leverage and therefore increases your risk. Past performance is not necessarily indicative of future results.

Recent Comments